Flexibility Comes Standard

Private lending is a very popular asset class with many possibilities. As the private lender for a property, you’ll actually function as the bank. In this example, let’s say you have $100,000 in a Rollover (aka Traditional) IRA and you want to loan it to an investor as a first mortgage on a property worth $135,000.

In this case, we’re looking at an LTV – Loan to Value – of 75%. Now I’ve had individuals come up to me after presentations very upset with the fact that there was a 75% Loan to Value, but this is just an example; I’m not actually telling you to do 75%.

The two parties – the lender(s) as well as the borrower – have agreed to a 9% interest rate. It’s going to be interest-only payments over five years, so we’re not amortizing the loan. To make it really clean and easy, we’ll keep it as a straight interest-only payment.

This is going to involve the regular closing that we’re used to as real estate investors. We’re simply going through a typical closing. All of the parties may or may not be there, but everything’s going to be recorded and the original documents are going to be held in a fireproof safe at American IRA’s office.

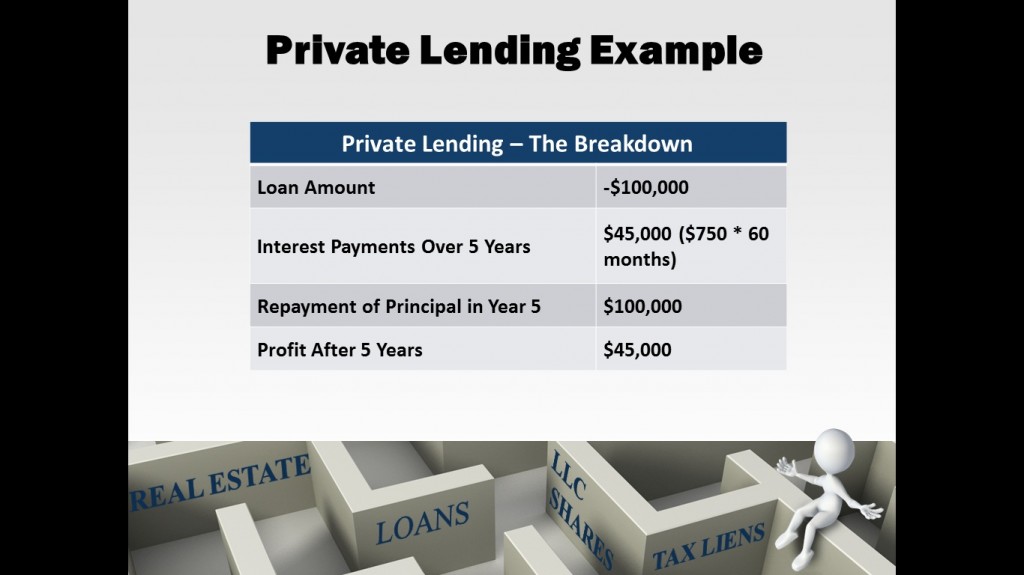

As you can see, we’re not making the decisions. You’re directing us regarding how and when you’d like to make the investment each step of the way. In this case (because it’s a traditional IRA) the interest is going to be tax-deferred in monthly quantities of $750. That’s just 9% of $100,000 broken down into monthly payments.

You’ll be able to see the incoming cash flow from the investment via your online statement. While we send out one paper statement each year, certainly feel free to observe the inflow and outflow of cash as it pertains to your account online.

At the end of the five years the loan is repaid; the interest accrued is $45,000, and the principal is repaid in full.