Your 401k Affects Your Self-Directed IRA

Retirement planning has something in common with pharmacology: Just as a doctor needs to understand how certain drugs may interact with one another, retirees and those who help clients plan for retirement should also understand how assets in different kinds of retirement accounts, or participation in a workplace plan such as a 401k, 403b or a defined benefit pension plan affect one another as how your 401k affects your Self-Directed IRA.

Retirement planning has something in common with pharmacology: Just as a doctor needs to understand how certain drugs may interact with one another, retirees and those who help clients plan for retirement should also understand how assets in different kinds of retirement accounts, or participation in a workplace plan such as a 401k, 403b or a defined benefit pension plan affect one another as how your 401k affects your Self-Directed IRA.

Background

Back in 1974, when Congress first passed ERISA, or the Employee Retirement Security Act – the law that authorized the IRA as we know it – they wanted the tax benefits to accrue primarily to people who, for whatever reason, were left out of the employer pension plan safety net. Of course, that safety net was much more robust in 1974 than it is now. At any rate, since Congress was giving up some current revenue and subsidizing retirement savings in IRAs in the form of an income tax exclusion, they wanted to focus that subsidy on those who needed it most: People who had no pension plan at work to fall back on.

They also wanted the benefits to accrue mostly to lower-income and middle-class families. The wealthier, it was thought, could take care of themselves with or without IRA contributions.

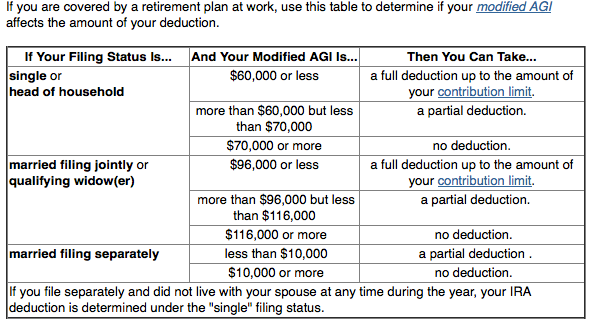

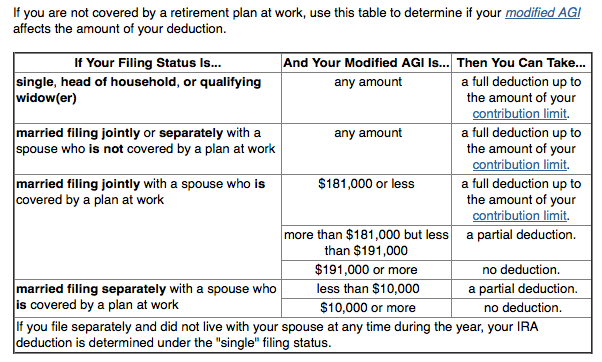

And so in order to meet these objectives, Congress came up with a scheme to set limits on who could deduct or exclude amounts contributed to IRAs from their income: Those who had a retirement plan at work had lower limits on allowable deductible contributions than those who didn’t. Furthermore, higher income individuals had their ability to deduct contributions restricted or denied altogether.

While over time the numbers have been adjusted to account for increases in the cost of living, we still have the same system in place for traditional (non-Roth) IRAs: You can contribute more on a deductible basis if you are not covered by a retirement plan at work than if you are. If your income is above a certain level, you may have your ability to deduct contributions restricted. You can, still, however, make non-deductible IRA contributions even if you fall above the income thresholds, up to the maximum total IRA contribution limit, which in 2014 is $5,500. Those age 50 or older can make an additional $6,000.

2014 Contribution Limits

As we mentioned, there are two tables defining allowable contribution limits. If you are covered by a retirement plan such as a 401k, you have to use the more restrictive of the two tables.

Note: These are the limits for 2014. If you’re reading this blog post after April 15, 2015, see www.irs.gov for the updated contribution limits, as appropriate. Note that for IRAs, you have up until April 15th of the following year to make contributions to an IRA for the previous year. This is different from the 401k deadline: If you are a 401k plan sponsor or contributor, you must complete all your contributions prior to January to have them count for the year.

Note as well that if both you and your spouse are not covered by a retirement plan at work, there are no phaseouts to worry about – you can contribute up to your maximum annual limit – again, $5,500 for 2014 – and double that for married couples, since you can make a spousal IRA contribution, as well. And don’t forget about the extra $1,000 ‘catch-up’ contribution.

Also, don’t let the income limits discourage you. Even if your modified adjusted gross income reaches the income phaseout limits, you can still make contributions to a traditional IRA on a non-deductible basis, provided you have at least that much in earned income.

So you can still get the benefit of tax-deferral on compounding and interest, plus the creditor protection features of IRAs, even though you don’t get the deduction on the contribution itself. Be sure to fill out an IRS Form 8606 if you make non-deductible IRA contributions so you will get credit for the taxes you did pay on money you contributed. Otherwise the IRS might not credit you properly and you will wind up paying needlessly higher taxes when you take the money out.

Since Your 401(k) Affects Your Self-Directed IRA, Many People Ask Whether They Can Max Out Both

In theory, contributing to your IRA does not limit your ability to contribute to your 401k plan, nor vice versa – though you may not be able to deduct some or all of your IRA contribution.

Roth IRAs and 401(k)s

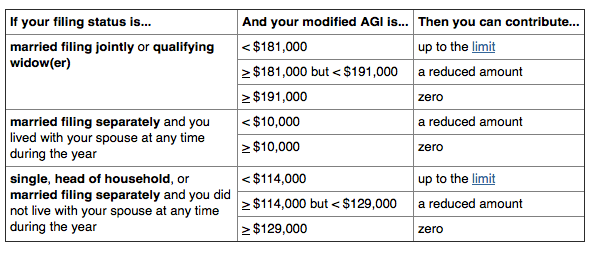

Roth IRAs work differently than 401ks. Since the IRS is still getting its tax revenue on money you earned that you contribute to a Roth IRA (Roth contributions are not tax-deductible), then the original thinking when Congress passed ERISA doesn’t apply. Consequently, Uncle Sam doesn’t care if you also have access to a retirement plan: They are quite happy to let you contribute the maximum $5,500 annual limit (again, add another $1,000 in ‘catch-up’ contributions if you are age 50 or older), no matter what kind of plan you have at work. Contributions to or eligibility for a workplace retirement plan has no effect whatsoever on the amount you can contribute to a Roth IRA. The only factors are your earned income, which must be sufficient to cover the contribution to the Roth IRA, and your overall modified adjusted gross income as defined here:

If you have more questions about how your 401k affects your Self-Directed IRA, call us today at 866-7500-IRA (472), or visit us at www.AmericanIRA.com. We’ll be happy to help!

Image by: presentermedia.com

Plan")