America’s Five Favorite Self-Directed IRA Investments

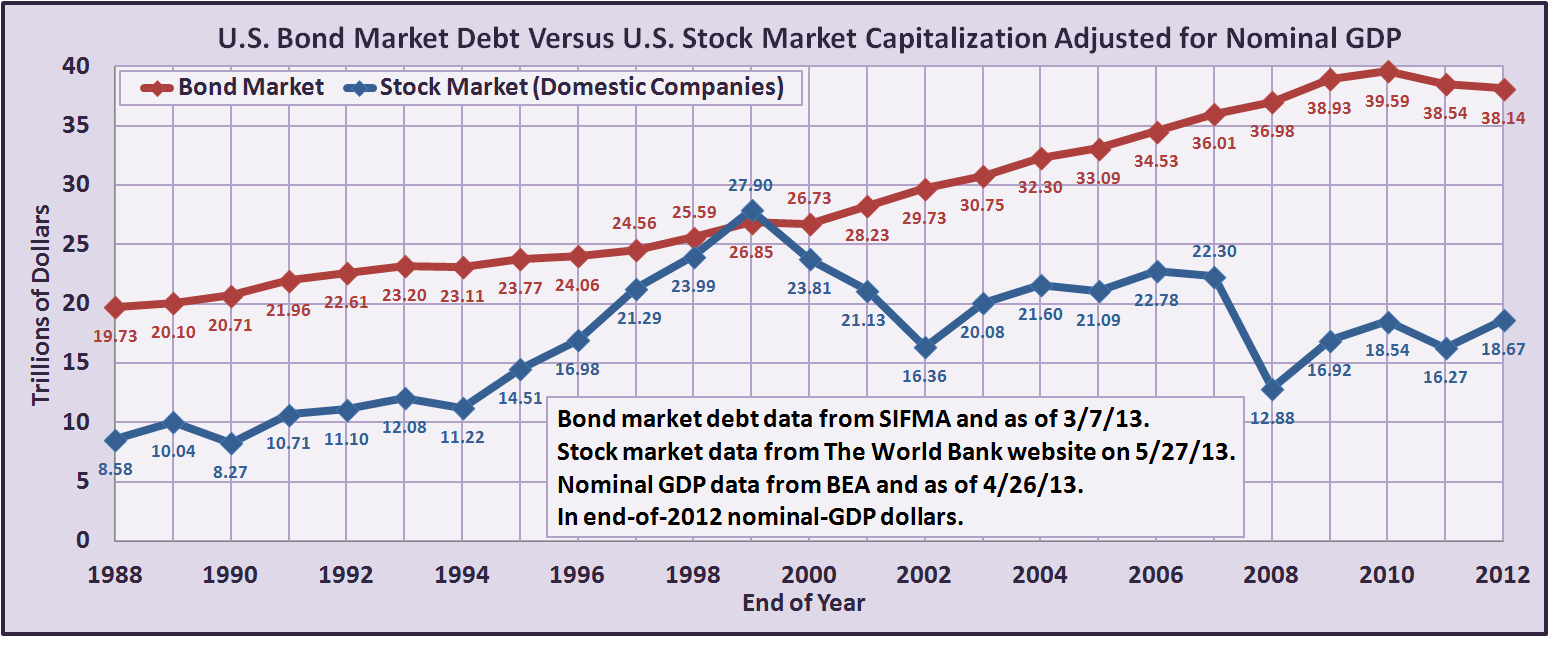

Bonds.

Yes, everybody likes to think of stocks, and stocks get all the glamor on cable TV shows like Squawk Box. But bonds are the 800-pound gorillas of the Self-Directed IRA investment world.

The total amount of outstanding bonds dwarfs the publicly traded stock market: As of 2012, there was $38.14 trillion worth of bonds floating around just in U.S. corporate and government debt alone. In fact, the only time the total U.S. stock market capitalization even approached the global bond market – and exceeded it, very briefly – was at the very peak of the Internet stock market bubble in 1999 and the first part of 2000 – when the Nasdaq was trading at over 100 times earnings.

Source: Learnbonds.com

A bond, of course, is simply an IOU issued by an entity – a corporation, association, domestic or foreign government – that borrows money. You can buy bonds from corporations, bonds representing a share of a pool of mortgages, or car notes, or credit card debt, or a right to future streams of revenue from a toll bridge. Even money market funds consist almost entirely of bonds-very safe bonds of short maturity, yes, but bonds nevertheless.

The chief source of bond return is usually interest, but bond prices fluctuate, as well, and you can enjoy gains or suffer losses from bond price movements as well. Want to own the whole global bond market? The quickest way to index it is to own shares in a Barclays Global Bond Aggregate ETF or index fund.

Stocks

Stocks, of course, represent an ownership interest in a corporation and stocks can be held as a Self-Directed IRA investment. If you own a share of stock, you simply own a claim on future earnings of a corporation. As of this writing, the most well known of stock market proxies – the Standard and Poor’s 500, is trading at about 19.84 times the current total earnings of the 500 biggest U.S. companies (as measured by the value of outstanding stock, or ‘market cap.’ That means if you buy a share in an index fund, you’re spending about 20 bucks for each dollar of earnings this year.

Is that a good deal? Only time will tell. Right now, the price of a dollar of current earnings is well within the historical trading range of the index, and even perhaps a bit on the high side – especially since the current dividend yield of the S&P 500 is very low, by historical standards, at 1.87 percent.

Real Estate

Real estate may fare somewhat better than large-cap stocks – at least on the dividend level. This is because real estate is generally designed to generate better cash-on-cash returns and is among the favorite Self-Directed IRA investment classes. Broadly speaking, the current cash dividend yield on real estate as measured by a broad index of real estate investment trusts is 4.08 percent – or over twice that of the S&P 500.

Individual investors can do much better, of course – by focusing on individual properties that can be bought quite cheaply, and by leveraging – so that a dollar invested buys the yield on two, three, four or more dollars! Naturally, the more leverage you use, the more you can possibly lose on your position as well. However, real estate has the advantage of being – well – real estate. That is, it’s not made of paper, like a bond or a stock certificate. Real estate rises and falls, of course, but unless you’ve bought an island that disappears in a volcanic eruption, it’s not going to fall to zero (and even then, you can sell mineral rights, which have value as well!)

It is possible to hold real estate – even interest in individual rental residential or commercial real estate properties – within a retirement account like an IRA, Solo 401(k), SEP or SIMPLE if you choose to self-direct and follow a few basic rules. To learn more, contact us and request a free guide to real estate investing within your retirement fund!

Gold and Precious Metals

Gold – together with its cousins of lesser glamor – silver, platinum and palladium – have been safe havens and stores of value in crises since the dawn of recorded civilization. These metals are beautiful, practical and quite scarce – and despite thousands of years of aggressive mining they’ve remained a scarce and valued commodity around the world.

Don’t expect gold or the other metals to pay a dividend. Really, they’re hunks of metal. They just sit there, until someone wants to trade them for something. But during times of crisis, when people lose faith in the staying power of currencies, governments and even whole civilization, these precious metals tend to kick into high gear.

As with real estate, you can hold them in a tax-advantaged retirement account, but you have to follow certain rules – and you can’t hold them directly. Again, contact us for a free guide to investing in gold and precious metals within your IRA. We’ll be happy to send it to you, no obligation.

Small, Closely Held Businesses

Americans love the small business man, and small business ownership has long been part and parcel of the American dream and an inspiration for untold millions.

They can be a lot of work, and risks are high. But so is the potential payoff for those who are successful. In fact, the potential profit of a successful small business is much, much greater than anything available in the highly-regulated world of mutual funds and annuities, for example. You can own shares in an individual publicly-traded stock, but unless you have a lot of shares, you won’t have much control. Your returns are dependent on the good faith and judgment of people who are almost always total strangers.

By sticking with very small businesses you can run yourself, you remain in full control. Furthermore – remember the 19.84 times earnings valuation of the S&P 500? Well, you can frequently buy very small family-owned businesses, like tire shops, restaurants, insurance agencies, and the like for anywhere from three to seven times earnings – or just a fraction of the cost of buying into the large-cap stock market. And again, you can do so while preserving the tax advantages offered by an IRA, Roth IRA, SEP, SIMPLE or 401(k). You can also own these businesses in a variety of forms, including as C corporations, LLCs, partnerships and joint ventures.

Want to learn more? Visit us at www.americanira.com, or call us at 866-7500-IRA (472). You can download any of our popular guides, or our valuable, exclusive e-book. We look forward to hearing from you.