Self-Directed Real Estate IRA Corner: How Much Should You Have Saved by Now?

Experienced Self-Directed IRA investors know: You need to monitor your investments, and how they perform over time. This is true with any individual security, and it is true with a Self-Directed Real Estate IRA rental property: If you own a house as a Self-Directed Real Estate IRA investment, you would want to know, how is it holding up to the elements? Is the roof in good repair? Is the wiring up to the demands of the modern household? Is the plumbing in good condition? Is it reasonable to expect that the home will generate acceptable income and capital appreciation in the future?

Because if you fail to monitor the status of your investment, you will not know if it’s time to take some corrective action – fix the roof, for example – until it’s too late and the damage is irreparable.

The same is true of an individual’s retirement portfolio as a whole. It’s important to take some vital signs from time to time, to ensure that your total retirement portfolio is in good shape, and that you are making acceptable progress toward your goal: An investment portfolio that is sufficient to continue to generate adequate income and financial security when you leave the work force.

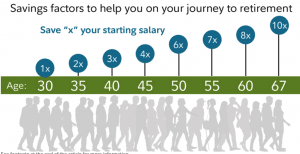

Fidelity Investments – the Boston-based mutual fund behemoth, came up with a useful concept that may make it easier for you to check your progress toward a successful retirement: Their analysts estimate that the minimum amount an individual should have saved by the age of 67 should be about ten times his or her annual income.

This, combined with Social Security, should be enough to see most people through, if they’re careful about expenses.

Well, if you know your target is 10 times your income at age 67, then it’s possible to work backwards from that number, given reasonable savings rates and assumptions about expected future returns over time, to arrive at a target multiple for other ages, too.

Here’s what Fidelity came up with:

If you want to be on track to hit that 10 times income multiple at age 67, then you should be hitting the other guideposts along the way:

Save your income by age 30, and twice your income by age 35. Save triple your income by 40, and so on.

Fidelity’s analysts calculated that this is very doable, for those who contribute at least 15 percent of their incomes to their 401(K)s beginning at age 25 – just a couple of years out of college.

If you got a late start, or if you are falling behind, then you’ll need to take some corrective measures. Specifically, you are probably going to need to take some combination of these actions:

- Increase the amount you are saving each year.

- Increase your annual expected returns (but this probably involves taking on more investment risk).

- Reduce the amount of unnecessary fees and expenses you’re paying within your retirement account.

- Reduce your lifestyle expectations in retirement.

Nearly everyone falls behind at one point or another. Some fall behind because of bear markets. But these can be great opportunities to increase your retirement savings contributions, because you can buy great assets at big discounts. They are also great opportunities to increase your annual expected returns: Those who moved heavily into Self-Directed Real Estate IRAs and stocks in 2009-2010, for example, made profits that substantially exceeded the long term returns of either the S&P 500 or the residential real estate market – simply because they bought at the bottom.

And as Warren Buffett points out in this great speech to Columbia University students, buying assets everybody else thinks of as “risky” at the bottom isn’t necessarily so risky at all.

That’s where Self-Directed IRA investing can play an important role: You want to buy assets that are on sale – that sell at low prices compared to their intrinsic value or discounted expected future income streams. But those are not always publicly traded securities. Stocks and bonds are both pretty expensive these days, as are most mutual funds that rely on them.

A Self-Directed IRA does not limit you to publicly traded securities. Those are the securities that Wall Street wants to sell, anyway.

Instead, using a Self-Directed IRA (or Self-Directed Solo 401(K), Self-Directed SEP IRAs, Coverdell education savings accounts and health savings accounts for that matter) let you combine the tax advantages you get with IRAs with the freedom to diversify into any asset class you like (except life insurance, jewelry/gems, alcoholic beverages and collectibles).

This also helps you increase expected returns without taking on much more risk with your overall portfolio: Adding alternative asset classes like rental real estate, tax liens and certificates, private lending, farm and ranchland, LLCs, partnerships and other common Self-Directed IRA investments can help cancel out volatility in other areas, smoothing overall portfolio performance without forcing you to ‘pull in your horns’ by buying low-risk, low-reward assets such as money markets and other cash equivalents.

Interested in learning more about Self-Directed IRAs? Contact American IRA, LLC at 866-7500-IRA (472) for a free consultation. Download our free guides or visit us online at www.AmericanIRA.com.